United States fintech Current Introduces high-yield savings account where customers earn 4.00% APY

United States fintech Current Introduces high-yield savings account where customers earn 4.00% APY

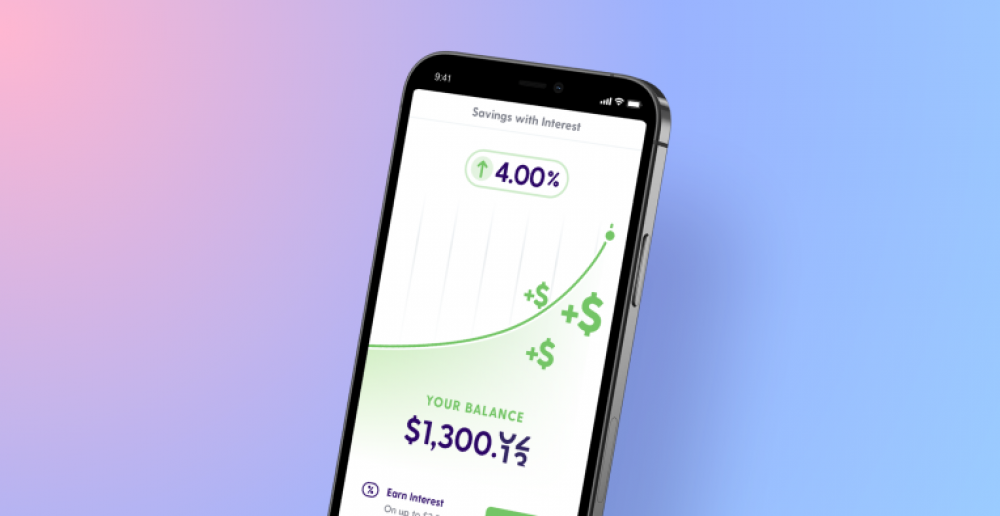

As competition among digital banks intensifies, US fintech Current is introducing a new product designed to improve the appeal of its banking service. The company announced this morning that it is launching a new high-yield product called "Interest" that will allow any Current account holder to earn a 4.00 percent Annual Percentage Yield (APY) — a rate that the company notes is 60x higher than the national average.

Interest will be available to all Current users, including those on the free Basic plan and those who pay for upgraded features. (In fact, the latter group likely contributes to Current's ability to increase its APY, as Premium subscribers pay $4.99 per month for Current's expanded service.)

While it is common for neobanks to offer a higher annual percentage yield (APY) than traditional banks, many banking services require users to jump through additional hoops to qualify for the higher rate. For example, One Finance offers a 1.00 percent annual percentage yield on funds up to $5,000 in its "Save" product, but you must activate the auto-savings feature to receive the higher 3.00 percent rate. Aspiration and Varo both offer a 3.00 percent annual percentage yield, but each has its own set of requirements regarding spending, balances, and total direct deposits.

Current's new offering, on the other hand, pays interest on funds up to a maximum of $6,000 per year, the company says. Additionally, it notes that there is no minimum balance requirement and no requirement for direct deposit or spending. However, what differentiates its product is that all members will be able to earn daily interest on their funds.

Attractive option for customers who are just beginning to save

Likewise, Current's product has a catch in that the $6,000 total must be spread across its Savings Pods. As a result, the APY is earned on amounts up to $2,000 per pod. This makes it a more attractive option for customers who are just beginning to save and want to organize their funds into distinct categories, rather than for those looking to park a larger balance.

Current tells TechCrunch that it is not introducing this high-yield product at a faster rate than it intends to reduce later.

"We are not approaching this as a promotional rate," explains Josh Stephens, Current VP of Product. "We're approaching it as something that will be available indefinitely... I'm sure you've seen promotional rates from other businesses with a lot of bells and whistles attached. However, this is something that is available to anyone, with no minimum balance requirement and no fees," he explains.

In addition, the company views the rate as a way to differentiate its banking service in a crowded market. Current began as a teen banking service and has grown to offer a more competitive product for adults — including those without children — over the years. Current, like many other digital banking services, offers perks such as no-fee overdrafts, cashback, fee-free ATM withdrawals, faster direct deposits, automated savings, and money management tools. With the launch of Interest, it is now also responding to customer demand for improved savings products.

"Over the last couple of months, inflation has risen at one of the fastest rates in 40 years. The Consumer Price Index has increased at the fastest rate since the early 1980s," Stephens notes. "And for our members — and for a large proportion of Americans — this means their money is not going nearly far enough. This implies that they are paying more for comparable goods and services. It makes it more difficult to save money."

Difficulty for banking customers to grow their money meaningfully

Meanwhile, Current believes that the market's current offerings make it difficult for banking customers to grow their money meaningfully.

The change may persuade some banking customers who currently have their funds in other savings accounts to switch to Current's service. They may eventually upgrade to premium Current products and services, making the higher APY economically viable.

Current now has over 3 million members, both free and paid, with an average age of 27 — younger than many of its competitors.

In the long run, the company intends to expand its offerings to assist these customers in further growing their money. It intends to enter the cryptocurrency space, having announced a partnership with Acala last year to develop a new category of "hybrid finance" that combines the benefits of traditional banking and decentralized finance. Consumer lending is also on the company's agenda.

Current's new Interest product is now available on iOS and Android.